2020 Pandemic: How might it change the ways we pay?

2020 Pandemic: How might it change the ways we pay?

Although the total number of payments in the Australian market is currently suffering a severe decline, as economic activity is strongly curtailed, what might happen to the ways consumers pay after the 2020 pandemic? Guest writers, David Oierholm and Lance Blockley of The Initiatives Group, offer their view.

The COVID-19 2020 Pandemic is having an unprecedented impact on how we live and work. We are planning for the worst and hoping for something better. No matter how long it takes for the crisis to pass, 2020 will be a year that is not forgotten quickly.

It will undoubtedly be a period of change, some of which will alter the way we do things forever.

We are likely to wash our hands more frequently, and we will be much better at conducting remote meetings using platforms such as Zoom, Webex, Skype for Business, GoToMeetings, etc. Telemedicine will likely become more prevalent, as will the ability and propensity to work from home effectively.

We will be super-sensitised to microbes, and, given the economic impacts being experienced, we may be more concerned about the sustainability of the companies we buy things from, together perhaps with more conservative views regarding our ongoing employment and income. Indeed, the cross-border supply chains that have been constructed over the last 15+ years of globalisation have been shown to be a potential weakness (e.g. a key global production site of surgical masks being in Wuhan), so perhaps domestic manufacturing will get a boost everywhere and cross-border commercial transactions decline.

Although the total number of payments in the Australian market is currently suffering a severe decline, as economic activity is strongly curtailed, what might happen to the ways consumers pay? Not necessarily in the short term – although many merchants are now refusing to take cash, travel card issuance & usage has crashed, and cross-border payments (a key revenue source for the international schemes) are drying up. Rather, we are looking at the potential longer term residual impacts.

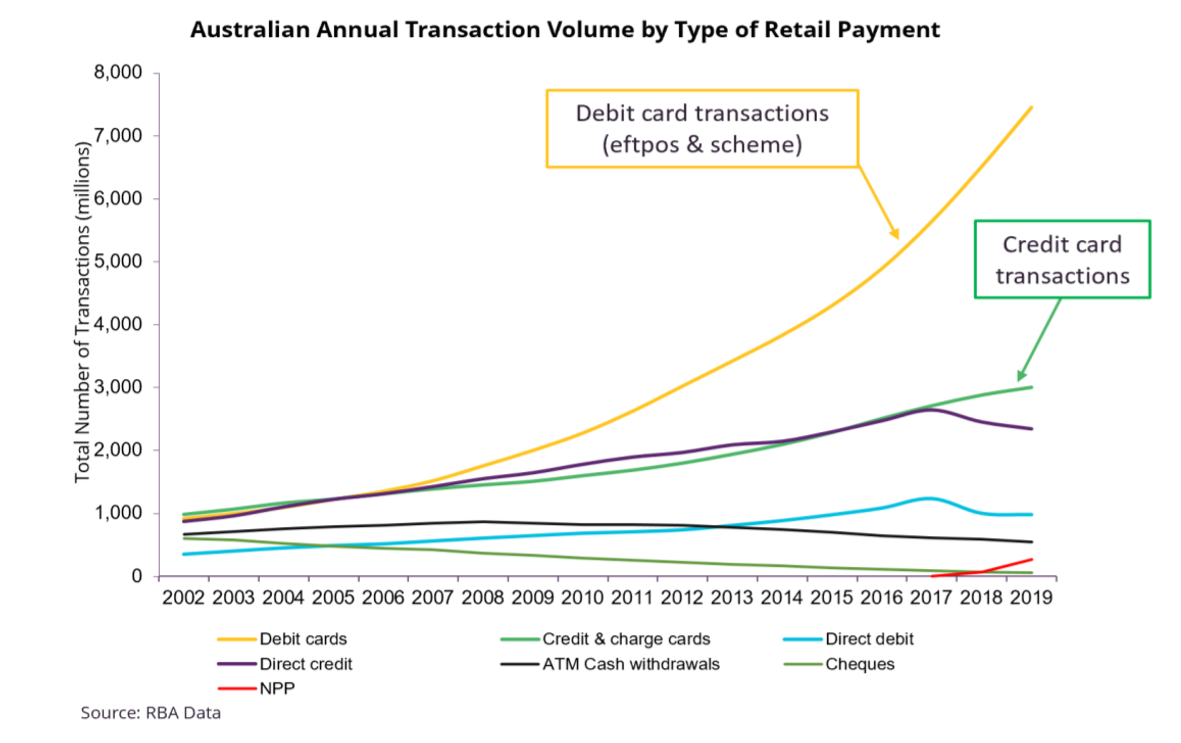

In The Initiatives Group white paper “The Changing Face of Consumer payments in Australia”, we identified that the way we pay takes a long time to change. It is all about trends, and long ones at that. The following graph was used to show how the ways we pay have changed over the past 15 years. The trends are clear – cash and cheques are on the decline, and fast becoming in the minority of transactions. Electronic payments continue to increase. Cards are now more than 60% of transactions, with the growth in debit cards far outstripping credit cards. It is now quite normal to pay for a morning coffee (currently only available as “take away”) using a card – not so long ago a $3.50 purchase would have been made with cash.

The trends are clear – cash and cheques are on the decline, and fast becoming in the minority of transactions. Electronic payments continue to increase. Cards are now more than 60% of transactions, with the growth in debit cards far outstripping credit cards. It is now quite normal to pay for a morning coffee (currently only available as “take away”) using a card – not so long ago a $3.50 purchase would have been made with cash.

What might happen to cash?

“Fed Plans Release of Clean Cash As Virus Spreads” (pymnts.com, March 22, 2020)

The decline in the use of cash will accelerate, along with an associated decline in ATM usage (noting that for every ATM withdrawal that does not happen, an additional 10-15 electronic transactions will be generated, mainly on debit cards).

Cash carries bacteria 1 (no prior studies seem to have focused on viruses!). Both cash and bacteria travel fast. Even though it has been found that polymer notes, like those used in Australia, carry less bacteria than (absorptive) paper notes such as those in the USA and China, consumers and merchants alike will be less keen on handling cash, and more keen on using electronic payments. Indeed, the UK has just lifted the contactless limit from GBP30 to GBP45 to help further reduce the use of cash. More locally in Australia, one of your authors has found that cash is no longer accepted at the local Coles Supermarket, Harris Farm Markets and the golf club (which is closed for now anyway).

Cash carries bacteria 1 (no prior studies seem to have focused on viruses!). Both cash and bacteria travel fast. Even though it has been found that polymer notes, like those used in Australia, carry less bacteria than (absorptive) paper notes such as those in the USA and China, consumers and merchants alike will be less keen on handling cash, and more keen on using electronic payments. Indeed, the UK has just lifted the contactless limit from GBP30 to GBP45 to help further reduce the use of cash. More locally in Australia, one of your authors has found that cash is no longer accepted at the local Coles Supermarket, Harris Farm Markets and the golf club (which is closed for now anyway).

So, are plastic cards the answer?

Australians are the world leaders in the use of contactless open-loop payments, with well in excess of 90% of card present transactions being contactless. This means that, for transactions under $100, we don’t need to touch a terminal that somebody else has used or handed us. We also don’t have to hand our card over to a stranger. That’s good, right?

Well, maybe not… unfortunately there are studies, albeit in the USA, where contactless payments are still in their infancy, that have shown that cards “can be grimier than cold hard cash”.2

However, it still feels safer to use a card that only you have held than notes and coins that have gone through multiple hands, so plastic cards will quickly pick up transactions from cash.

How about other transactions that use the card rails?

Mobile Wallets

Despite the high ownership of smartphones and Australians’ love of contactless payments, until recently, the take up of mobile wallets such as Apple Pay, Google Pay and Samsung Pay (the “Pays”) has been slow. It may depend on your industry and your demographic, but The Initiatives Group has heard conflicting reports. Claims of 25% of POS transactions being handled via the Pays have been offset by merchant claims of far far lower percentages, hence we would suggest that the average across all contactless payments is still under 10%.

Regardless, the use is set to accelerate. Your phone may or may not be a great carrier of bacteria, but it is something you will touch anyway, so what’s the difference if you now use it for payments and avoid fiddling around with your wallet for a card.

Wearables

Whilst wearables are only another form factor for using the Pays, their use is likely to increase as an even more “contactless contactless” form of payment. Notwithstanding we believe that wearables, perhaps other than smart watches, will remain relatively niche.

In-app payments

In-app payments are likely to be a big winner from the COVID-19 crisis. Seamless payments will be the most contactless of contactless payments. Whilst in the short-term popular use cases such as Uber transport will take a significant hit, there will be many new use cases that become available earlier or even more popular – think of ordering home delivery (from supermarkets, for prepared food e.g. Menulog, Ubereats) and petrol stations (where something like the Caltex app avoids the need to enter the shopfront). We will be more ready to form new “safe” habits, and, if used frequently enough, these use cases will be habit forming, just as the adoption of contactless card payments was slow until Woolworths and Coles offered them (back in 2012).

We found the new 13cabs “No Touch Parcel Deliveries” of interest. Whilst no-touch may not be as big a deal from 2021, here is another reason to get into the habit of using in-app payments for taxi services. In the future will we see the groceries delivered paid within the 13cabs app, or the taxi delivery paid for within the Coles or Woolworths app?

Peer to peer payments

As handling cash becomes less popular, might we now see electronic peer to peer payments use accelerate. Perhaps this will provide stimulus to the use of PayID, Beem It and card-tocard systems. Although current social distancing and work-fromhome orders may well diminish the need to pay our friends and relations in the near term.

eCommerce card not present

In the short-term, eCommerce spend on travel and discretionary items has tanked, however online ordering of grocery goods and fresh foods is up globally. Discretionary spend, such as fashion, will recover once people are again allowed to physically interact. Grocery and fresh food ordering online will be a new habit – whether for home, work or locker delivery, or click and collect. Although it may not maintain at COVID-19 levels, this will likely fuel more rapid long term growth in eCommerce retail spend.

Monthly payments

The economic impact of potential (or actual) unemployment, of recession and of media noise about depression, will all make consumers more wary of both the sustainability of companies that they deal with and their own ability to pay in annual large lump sums. We predict this will lead to a preference for annual payments to be made monthly (already a trend before the crisis), and not necessarily by auto direct debit (as consumers may wish to retain control). In addition, this preference may lead to consumers demanding that they are not penalised with any surcharge for paying monthly.

Noting that, just as the decline in ATM use accelerates the volume of electronic payments, so too does monthly payment . . . 12 transactions rather than one.

New products

Adversity is often the mother of invention, so it is likely that we will see a range of new electronic payment products, use cases and services being created.

Opportunities only for the card rails?

An emphatic “No”. As noted above, online real-time payments over the NPP may be accelerated – whether by Osko, other overlay services or by ‘pay anyone’ (previously via direct entry) payments growing faster. The increased volumes allowing the NPP to become less expensive per transaction.

Perhaps a trend towards mobile phone payments will improve the use case for NPP payments on your phone at POS, enabled by QR codes? Notwithstanding, we do expect that there will be even more new overlay service activity that takes advantage of the NPP.

Conclusion – How might Covid 2020 Pandemic Change the Way We Pay?

The current COVID-19 crisis will see payment volumes drop sharply as economic activity stalls. Within the remaining payment activity, the mix of payments will change:

- The reduction in cash and ATM usage that has been occurring over many years will accelerate into a steep decline

- The cross-border usage of payment cards will drop to low levels

- Use of contactless card and mobile payments will rise

- Use of remote services/ordering, and with them the associated remote payments (eCommerce, in-app, other online), will increase

- A move to monthly payments.

Depending upon the length of the crisis, many of these changes will become habitual and are likely to outlast the short term impact of the virus – such that the retail payments mix in the Australian economy will be altered forevermore.

Disclaimer: The opinions expressed in this article are the author’s own and do not necessarily reflect the view of Indue. The Initiatives Group has advised participants in the payments market since the 1990’s – including issuers, acquirers, third-party processors, technology providers and associations. The Initiatives Group has a strong relationship with Indue, and can help participants in the payments sector generate more value from their markets and customers. To find out how, please get in touch.

Sources:

1 A Oxford University study in 2014 found that the average European banknote contained 26,000 bacteria which could be potentially harmful to a person’s health; and market research has found the majority of European consumers rank physical money as being more unhygienic than the hand rails on public transport

2 https://www.fastcompany.com/90480199/how-companies-can-support-their-employee-caregivers-duringthecovid-19-outbreak