Top three 2020 financial crime trends

Top three 2020 financial crime trends

The global pandemic and subsequent economic downturn has presented a new set of challenges for financial institutions

The global pandemic and subsequent economic downturn has presented a new set of challenges for financial institutions as they work to keep pace with financial crimes across the sector. With advancements in technology, changes in human behaviour and an increase in vulnerability as a result of COVID-19, it has never been more important for organisations to remain ahead of the financial crime curve and put up a solid defence in a post-pandemic world.

As the nation continues to navigate the ‘new normal’, we took a look at the top three financial crime trends of 2020 with Indue’s Financial Crimes team as a friendly reminder to stay vigilant and safeguard against professional perpetrators.

1. Rise of ecommerce

There’s no doubt the way we choose to pay has materially changed since the onset of COVID-19. With lockdown restrictions across the country, we’ve seen traditional brick and mortar stores exchanged for convenient and contactless ecommerce channels.

As a result, ATM withdrawals and cash-out transactions have dropped considerably, with the RBA reporting a 52% and 30% decrease respectively for the quarter ending June 2020.

Meanwhile, a recent report by Australia Post revealed ecommerce has grown by a mammoth 80% year on year in the eight weeks since COVID-19 was declared by the World Health Organisation, with an average of 2.5 million households buying something online each week in April 2020, compared to 1.6 million in 2019.

This significant shift to online transactions has seen a corresponding increase in online fraud. Indue’s Head of Financial Crimes, Dean Wyatt, said the company’s internal fraud metrics in relation to ecommerce had reported a 28% rise to 98% since the global pandemic hit.

“With an increase in online traffic comes an increase in fraud associated with ecommerce merchants, putting customers’ personal details at risk,” he said.

“On the other hand, we’ve seen instances of petty theft and stolen cards decline as a result of restrictions such as curfews and people generally travelling less, including people shifting to working from home arrangements.

“The good news is we’ve been able to hone in on this change using our multi-channel Orion Financial Crimes service, and align our analytics to identify and track suspicious behaviour in real time, to ensure our customers remain protected.

“Customers need to be aware that if they’re using new types of payments, they need to be following the same rigor as you would when paying instore.”

2. The art of social engineering

Social engineering by definition seeks to exploit human psychology to access and obtain personal information, and it’s this type of scam that continues to outsmart targets.

From phishing attacks (fraudulent emails or texts that appear to come from a reputable source) to baiting (a false promise to pique a victim’s greed or curiosity), the goal of the ‘social engineer’ is to trick individuals into giving up sensitive information or visiting malicious URLs to compromise their systems.

“We have seen a strong shift to perpetrators compromising people directly and involving them in the scam, rather than solely relying on targeting accounts or cards,” Dean said.

“Compromising identity details across driver licences, passports, and email or social media accounts is hot property at the moment because financial services are inherently integrated with those types of documents, information and platforms.

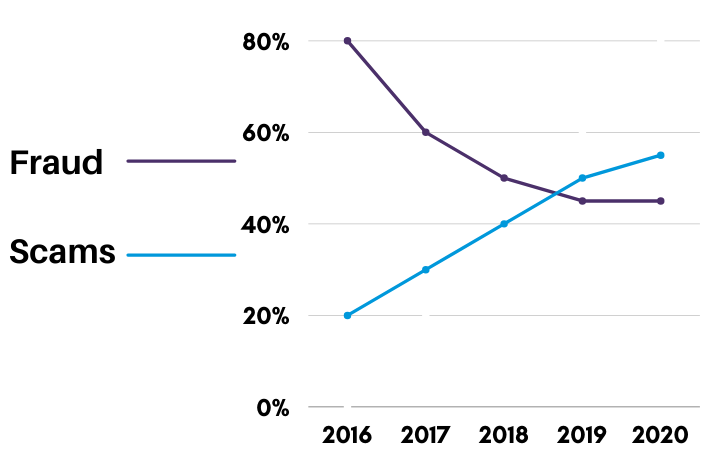

“People are fooled by sophisticated attacks that purport to ‘know you’, calling with pieces of information already collected, with the intention of gathering further details from the victim. When scammers are able to access detailed personal information, they can easily create new accounts or lines of credit under individuals’ names. “At Indue, we have seen a considerable rise in social engineering over the last four years, to the point where it is now a larger problem than fraud. In 2016, financial crimes represented 80% fraud compared to only 20% social engineering scams, but as of 2020, we’re now seeing 45% fraud compared to 55% scams.”

“At Indue, we have seen a considerable rise in social engineering over the last four years, to the point where it is now a larger problem than fraud. In 2016, financial crimes represented 80% fraud compared to only 20% social engineering scams, but as of 2020, we’re now seeing 45% fraud compared to 55% scams.”

According to the Australian Payments Network, the most common contact method for scam activity in Australia is by email, but scams via phone result in the most financial loss.

3. Money laundering and terrorism financing

A key focus for institutions and regulators has been the growing trend of traditional financial crimes, like money laundering and terrorism financing, with both AUSTRAC and the Financial Action Task Force (FATF) reviewing controls and payment systems to identify potential weaknesses that could be exploited by criminals across the sector.

Money laundering seeks to disguise the proceeds of crime as legal income, while terrorism financing, as the name suggests, funds terrorist activities, both of which have the potential to trigger global repercussions.

Tough financial penalties have been handed down in recent times — the Commonwealth Bank of Australia and Westpac have both been hit with fines totalling $2 billion relating to serious breaches of anti-money laundering and counter-terrorism financing laws.

“With the shift of payments to a digitized world, more criminals are taking advantage of the opportunity to leverage these methods and innovative ways of sending financial transactions to each other,” Dean said.

“The rise of financial crime and the importance of protecting payment ecosystems has never been more important. With AUSTRAC’s presence increasingly felt in Australia over the last few years, I see it remaining a consistent focus beyond 2020.

“Genuine customer behaviour is certainly playing into it as well — with a strong shift to online payments, criminals are increasingly moving from hard cash to online transfer methods and attempting to hide between the genuine customer activity.

“As part of our Orion Financial Crimes solution, our anti-money laundering and counter terrorist financing service monitors customer account behaviour and transactions for unusual patterns, to detect activity that may be reportable under the Australian Anti-Money Laundering and Counter Terrorist Financing Act.”

Find out more

Learn more about Indue’s Orion Financial Crimes service, a multi-channel detection system that harnesses transactional data, customer behaviour and biometrics to expose anomalies and identify fraudulent activity. Delivered by an expert team, the service is forward-thinking with a machine learning/artificial intelligence component and places customers ahead of the curve, providing a safety net when it comes to material risks and losses.

customer behaviour and biometrics to expose anomalies and identify fraudulent activity. Delivered by an expert team, the service is forward-thinking with a machine learning/artificial intelligence component and places customers ahead of the curve, providing a safety net when it comes to material risks and losses.

References

1. https://www.rba.gov.au/payments-and-infrastructure/resources/payments-data.html

2. https://auspost.com.au/content/dam/auspost_corp/media/documents/2020-ecommerce-industry-report.pdf

3. https://www.auspaynet.com.au/sites/default/files/2020-08/Fraud_Report_2020.pdf