From days to minutes: Payment services provider Indue accelerates its ability to innovate using Azure

Indue has been a significant player in Australia’s payments sector for more than 50 years. The payments technology provider is an Authorised Deposit Taking institution who specialises in helping organisations of all types adapt to and benefit from the latest innovations in payments technology.

Through its solutions – which encompasses everything from card management and mobile payments to direct entry transactions and real-time fraud detection – Indue aims to eliminate the need for multiple third-party engagements and streamline the payment system implementation process.

Indue is a founding member of Australia’s New Payments Platform (NPP), launched in February 2018 to modernise the nation’s payment infrastructure. The platform enables faster, more flexible and data-rich transactions to meet the evolving needs of Australian consumers, businesses and financial institutions.

Keith Bromwich, Head of Architecture at Indue, says Indue has helped clients adopt the NPP since its inception.

“Our role is to allow tier 2 and 3 financial institutions such as mutuals, regional banks and BAAS providers to access the NPP via our own platform,” he explains.

In June 2023, the NPP introduced PayTo, a new digital way for merchants and businesses to initiate real-time payments from their customers’ bank accounts. PayTo solves many existing challenges with direct debit payments, including processing delays, limited transaction information, and a lack of control for consumers and businesses over payments.

To ensure it could help clients adopt the new payment method, Indue embarked on an ambitious project in March 2022 to transform its technology infrastructure – largely made up of on-premise data centres – and adopt a more cloud-native approach.

In May 2022, Indue engaged Microsoft partner Arinco to help it develop enterprise-scale landing zones and a robust application programming interface (API) platform in Azure.

“The people we worked with at Arinco were absolute knowledge leaders,” says Bromwich. “They helped us make the right decisions by providing the pros and cons.”

Arinco used a flexible delivery approach to facilitate development timelines, which saw the first application landing zones for PayTo being implemented by early July 2022. This enabled Indue’s developers to build new capabilities for testing by October 2022.

As this was Indue’s first major deployment of modern web APIs in Azure, Arinco supported and educated Indue’s developers and engineers by leveraging its partnership with Microsoft.

“Firstly, we embedded consultants within Indue’s development teams, focusing on accelerating outcomes and providing best practice guidance for topics such as .NET development, Azure API deployment and security,” says James Westall, Account Executive at Arinco.

“Secondly, our consultants worked with Indue’s platform engineers, sharing our expertise with them as we developed code for each landing zone. This meant that at transition time, Indue engineers were starting from a solid knowledge base.

“Lastly, we partnered with Microsoft to deliver hands-on Azure Accelerate workshops. These covered key topics identified by Indue, enabling employees to get familiar with Azure in a safe environment with instructor guidance.”

The other challenge that Arinco helped Indue solve was the operational sign-off of its Azure capability.

“As an entity that’s regulated by the Australian Prudential Regulation Authority, Indue must be able to attest to the security, stability and robustness of its services,” explains Westall. “The deployment that we developed was designed to remain compliant using Azure and third-party security tools, including the capability to hold Payment Card Industry data.

“We also assisted Indue in developing several operational documents and procedures, ensuring key details about running solutions on Azure were available for external auditors.”

Arinco’s accelerated approach enabled Indue to launch its PayTo integration within the tight timeframe and begin onboarding clients in June 2023.

Enhancing innovation in the cloud

While Indue is still in the early stages of its cloud journey, its event-driven architecture in Azure is already delivering benefits. These include increased flexibility and scalability, which enable Indue’s developers and engineers to deploy any project – not just PayTo – in the cloud much faster and move from business idea to development workload in minutes or hours rather than days.

“The innovation piece is a key focus for Indue and its customers,” says Ryan Spain, Chief Information Officer at Indue. “Leveraging cloud-based technologies like Azure gives us access to a much wider variety of innovative capabilities in a fraction of the time compared to on-premise, and enhances the products and services we can offer.”

Indue’s move to the cloud has also helped them simplify its technology stack and reduce operational costs. Transitioning its Corporate Services (Virtual Desktop, remote access, and Office environment) to the Azure Virtual Desktop capability which operates within the enterprise-scale landing zone structure.

Now, key personnel can focus more on value-adding tasks rather than maintaining the performance and security of Indue’s hardware and software.

“We don’t have to worry about data centre connectivity or patching. All of that low-level maintenance is done by Microsoft,” says Bromwich.

Indue plans to grow its cloud footprint in Azure by kicking off two other major projects in 2023. One will focus on implementing a big data lake that leverages Microsoft’s advanced analytics capabilities. The other project will focus on migrating Indue’s on-premise Microsoft Dynamics 365 platform to Azure. Both projects will further enhance Indues’ ability to deliver innovative payment solutions and a better customer experience, according to Spain.

“This is a strategic partnership with Microsoft,” he says. “They’ve been on the journey with us from the start, and we really appreciate the assistance and guidance they’ve provided. The partnership has been a key enabler for facilitating both the PayTo integration and our broader cloud strategy.”

Source: Microsoft News 30 June 2023

Is the end of the cheque finally in sight?

Real-time, data-rich payment technology is transforming the way people pay for goods and services, consigning the once-popular paper cheque to dwindling niche sectors.

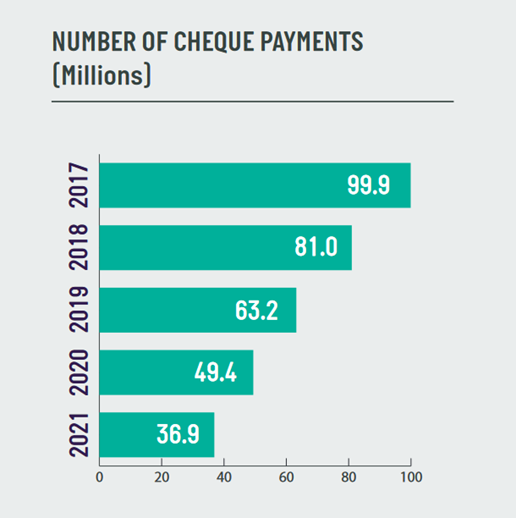

The end could finally be in sight within five years if cheques’ current decline in popularity continues, according to an AusPayNet report[1].

“Cheques are just clinging on,” says Grant Halverson, the chief executive of banking and payments firm McLean Roche Consulting.

“Most consumers have stopped using them except for some very infrequent types of payment. The biggest users are government departments, both state and federal, so when they’ll get rid of them cheques will be gone.”

Work has continued to amend legislation that specifies payment types, such as replacing the Pay Doctor via Claimant Cheque scheme in the Health Insurance Act with an automatic electronic funds transfer.

“Our analysis is that this will solve almost 75% of the government-related cheques issued,” according to AusPayNet.

COVID-19 accelerated digitisation of payments

The COVID-19 pandemic has also accelerated the trend away from cheques as lockdowns prevented in-person transactions and heightened the need to quickly distribute government subsidies.

Services Australia was the first government department to send relief payments in real-time via BPAY Group’s Osko system to those affected by the 2019-20 summer bushfires and COVID-19 disaster payments in 2020-21.

Osko allows payments to be made in seconds, including on weekends, and also includes far more detailed data about the payment.

These were key attractions of cheques in a largely pre-digital age, according to the RBA[2], given cheques could be written on a 24-7 basis and could include information (such as an attached invoice) to accompany the payment.

Source: RBA Payment Statistics

Charities leave cheques behind, BPAY a new choice

Charities have traditionally received millions of dollars in donations via cheques, particularly from older Australians.

Fundraising Institute of Australia (FIA) member data from 2019 showed that up to approximately 30% of fundraising revenue was received via cheques. The FIA wants to maintain cheques as a payment method although the pandemic has also encouraged older Australians to adopt digital payment methods.

More than three-quarters (77%) of Australians aged 65 and over were using online banking at June 2020 compared to slightly more than half (59%) just three years earlier, according to ACMA[3].

AusPayNet continues to work with industry bodies, including the not-for-profit sector and government, to increase awareness of the decline in cheques and of payment alternatives.

Meanwhile, some charities are now adding BPAY as a payment method, such as Rural Aid or Save the Children.

It allows the payer to confirm who they are paying at the time of payment, while the charity can issue the payer with a unique “Donor Number” as their reference.

“This makes it easy to reconcile the payment when it’s received, and they know who to send the tax receipt to,” says BPAY Group Managing Director Kim Tyler.

“Donors can also set up recurring payments using the same reference, while funds are received the next business banking day by the charity – they don’t need to wait for the cheque to clear.”

Property settlements go electronic

Another key reason for the rapid decline of cheques has been the adoption of e-conveyancing when buying a property.

Property settlement once required the buyer to hand over a bank cheque in exchange for the documents required to register them as the new property owner.

A PwC report commissioned on behalf of digital exchange PEXA estimated that up to five cheques were required per transfer and one additional cheque per discharge in 2015.

Now more than 80% of all property transfers and 95% of all refinances nationally are conducted over the digital PEXA exchange.

“The banks have enormous cost in creating and holding the cheque books,” Halverson says. “Everything about them is wrong: printing paper, the time it takes to turn them around, the cashflow you lose, and the lack of information.”

AusPayNet says it continues to monitor cheque usage into 2022, to ensure that current cheque users are not left behind as individual financial institutions ultimately make the decision that it is no longer a commercial decision to issue them.

[1] Future State of Payments Action Plan. Conclusions from AusPayNet’s Consultation. August 2020. Retrieved from https://www.auspaynet.com.au/sites/default/files/2020-08/APN_Future_State_Conclusions_Consultation_Paper_Aug20_0.pdf

[2] The Ongoing Decline of the Cheque System | Bulletin – June Quarter 2017. (2017). Reserve Bank of Australia. Retrieved from https://www.rba.gov.au/publications/bulletin/2017/jun/7.html#box-a

[3] The digital lives of younger and older Australians | ACMA. (2022, April 07). Retrieved from https://www.acma.gov.au/publications/2021-05/report/digital-lives-younger-and-older-australians

Source: BPAY Pty Ltd bpay.com.au (ABN 69 079 137 518).

A Look at Gen Z Banking Habits and Attitudes

Compared to other generations, fewer Gen Z customers expect to remain with their primary financial services organization a year from now. Do you know what Gen Z wants?

They are mobile-centric, diverse, ambitious and just starting their careers. They also have strong opinions on what they expect from their financial services organization. Our BAI Banking Outlook Special Report shares essential insights on Gen Z, the newest generation of banking customers.

Source: BAI 2022, www.bai.org

Biometrics to secure over $3 trillion in mobile payments by 2025

Biometrics to secure over $3 trillion in mobile payments by 2025

A new study has found that biometrics will authenticate over $3 trillion of payment transactions in 2025, from just $404 billion in 2020.

A new study has found that biometrics will authenticate over $3 trillion of payment transactions in 2025, from just $404 billion in 2020.

The report found that biometrics, including fingerprint, iris, voice and facial recognition are becoming critical to offering compelling app experiences, as mobile payments begin to take off in the payments landscape.

The extraordinary growth of over 650% will be fuelled by increased use of OEM Pays (such as Apple Pay and Samsung Pay), for both remote and in-store payments, as these applications have already embraced biometric authentication methods.

The research recommends that all payment apps take notice of biometrics and build the most seamless user experience leveraging biometric capabilities, or risk losing out to more secure OEM Pay alternatives.

Biometric usage lagging behind hardware adoption

The research found that although biometric capabilities will reach 95% of smartphones globally by 2025, only 35% of these smartphones will be used for making biometric payments in e-commerce in the same year.

The research identified that stored card-on-file payments without biometric security remain common in e-commerce, and that it will require significant efforts by stakeholders to transition spend to biometrically-secured methods.

“While biometrics are now an established part of the ecosystem, payments and e-commerce apps have not kept pace with the rate of innovation,” explains Research co-author Susan Morrow. “Merchants must adopt biometric capabilities rapidly and educate users to best secure the increasingly massive e-commerce market.”

Contactless payments driving biometrics use

The research also found that contactless mobile payments are a major driver of increased biometrics use, with the number of contactless mobile transactions secured by biometrics increasing by over 520% between 2020 and 2025.

The research identified contactless cards as the main threat, as they do not require the extra verification step, meaning that payment vendors need to incentivise wallet use to drive greater adoption of biometrics.

Source: Alex Rolfe – Payments Cards and Mobile 2nd February 2021.

2020 Pandemic: How might it change the ways we pay?

2020 Pandemic: How might it change the ways we pay?

Although the total number of payments in the Australian market is currently suffering a severe decline, as economic activity is strongly curtailed, what might happen to the ways consumers pay after the 2020 pandemic? Guest writers, David Oierholm and Lance Blockley of The Initiatives Group, offer their view.

The COVID-19 2020 Pandemic is having an unprecedented impact on how we live and work. We are planning for the worst and hoping for something better. No matter how long it takes for the crisis to pass, 2020 will be a year that is not forgotten quickly.

It will undoubtedly be a period of change, some of which will alter the way we do things forever.

We are likely to wash our hands more frequently, and we will be much better at conducting remote meetings using platforms such as Zoom, Webex, Skype for Business, GoToMeetings, etc. Telemedicine will likely become more prevalent, as will the ability and propensity to work from home effectively.

We will be super-sensitised to microbes, and, given the economic impacts being experienced, we may be more concerned about the sustainability of the companies we buy things from, together perhaps with more conservative views regarding our ongoing employment and income. Indeed, the cross-border supply chains that have been constructed over the last 15+ years of globalisation have been shown to be a potential weakness (e.g. a key global production site of surgical masks being in Wuhan), so perhaps domestic manufacturing will get a boost everywhere and cross-border commercial transactions decline.

Although the total number of payments in the Australian market is currently suffering a severe decline, as economic activity is strongly curtailed, what might happen to the ways consumers pay? Not necessarily in the short term – although many merchants are now refusing to take cash, travel card issuance & usage has crashed, and cross-border payments (a key revenue source for the international schemes) are drying up. Rather, we are looking at the potential longer term residual impacts.

In The Initiatives Group white paper “The Changing Face of Consumer payments in Australia”, we identified that the way we pay takes a long time to change. It is all about trends, and long ones at that. The following graph was used to show how the ways we pay have changed over the past 15 years. The trends are clear – cash and cheques are on the decline, and fast becoming in the minority of transactions. Electronic payments continue to increase. Cards are now more than 60% of transactions, with the growth in debit cards far outstripping credit cards. It is now quite normal to pay for a morning coffee (currently only available as “take away”) using a card – not so long ago a $3.50 purchase would have been made with cash.

The trends are clear – cash and cheques are on the decline, and fast becoming in the minority of transactions. Electronic payments continue to increase. Cards are now more than 60% of transactions, with the growth in debit cards far outstripping credit cards. It is now quite normal to pay for a morning coffee (currently only available as “take away”) using a card – not so long ago a $3.50 purchase would have been made with cash.

What might happen to cash?

“Fed Plans Release of Clean Cash As Virus Spreads” (pymnts.com, March 22, 2020)

The decline in the use of cash will accelerate, along with an associated decline in ATM usage (noting that for every ATM withdrawal that does not happen, an additional 10-15 electronic transactions will be generated, mainly on debit cards).

Cash carries bacteria 1 (no prior studies seem to have focused on viruses!). Both cash and bacteria travel fast. Even though it has been found that polymer notes, like those used in Australia, carry less bacteria than (absorptive) paper notes such as those in the USA and China, consumers and merchants alike will be less keen on handling cash, and more keen on using electronic payments. Indeed, the UK has just lifted the contactless limit from GBP30 to GBP45 to help further reduce the use of cash. More locally in Australia, one of your authors has found that cash is no longer accepted at the local Coles Supermarket, Harris Farm Markets and the golf club (which is closed for now anyway).

Cash carries bacteria 1 (no prior studies seem to have focused on viruses!). Both cash and bacteria travel fast. Even though it has been found that polymer notes, like those used in Australia, carry less bacteria than (absorptive) paper notes such as those in the USA and China, consumers and merchants alike will be less keen on handling cash, and more keen on using electronic payments. Indeed, the UK has just lifted the contactless limit from GBP30 to GBP45 to help further reduce the use of cash. More locally in Australia, one of your authors has found that cash is no longer accepted at the local Coles Supermarket, Harris Farm Markets and the golf club (which is closed for now anyway).

So, are plastic cards the answer?

Australians are the world leaders in the use of contactless open-loop payments, with well in excess of 90% of card present transactions being contactless. This means that, for transactions under $100, we don’t need to touch a terminal that somebody else has used or handed us. We also don’t have to hand our card over to a stranger. That’s good, right?

Well, maybe not… unfortunately there are studies, albeit in the USA, where contactless payments are still in their infancy, that have shown that cards “can be grimier than cold hard cash”.2

However, it still feels safer to use a card that only you have held than notes and coins that have gone through multiple hands, so plastic cards will quickly pick up transactions from cash.

How about other transactions that use the card rails?

Mobile Wallets

Despite the high ownership of smartphones and Australians’ love of contactless payments, until recently, the take up of mobile wallets such as Apple Pay, Google Pay and Samsung Pay (the “Pays”) has been slow. It may depend on your industry and your demographic, but The Initiatives Group has heard conflicting reports. Claims of 25% of POS transactions being handled via the Pays have been offset by merchant claims of far far lower percentages, hence we would suggest that the average across all contactless payments is still under 10%.

Regardless, the use is set to accelerate. Your phone may or may not be a great carrier of bacteria, but it is something you will touch anyway, so what’s the difference if you now use it for payments and avoid fiddling around with your wallet for a card.

Wearables

Whilst wearables are only another form factor for using the Pays, their use is likely to increase as an even more “contactless contactless” form of payment. Notwithstanding we believe that wearables, perhaps other than smart watches, will remain relatively niche.

In-app payments

In-app payments are likely to be a big winner from the COVID-19 crisis. Seamless payments will be the most contactless of contactless payments. Whilst in the short-term popular use cases such as Uber transport will take a significant hit, there will be many new use cases that become available earlier or even more popular – think of ordering home delivery (from supermarkets, for prepared food e.g. Menulog, Ubereats) and petrol stations (where something like the Caltex app avoids the need to enter the shopfront). We will be more ready to form new “safe” habits, and, if used frequently enough, these use cases will be habit forming, just as the adoption of contactless card payments was slow until Woolworths and Coles offered them (back in 2012).

We found the new 13cabs “No Touch Parcel Deliveries” of interest. Whilst no-touch may not be as big a deal from 2021, here is another reason to get into the habit of using in-app payments for taxi services. In the future will we see the groceries delivered paid within the 13cabs app, or the taxi delivery paid for within the Coles or Woolworths app?

Peer to peer payments

As handling cash becomes less popular, might we now see electronic peer to peer payments use accelerate. Perhaps this will provide stimulus to the use of PayID, Beem It and card-tocard systems. Although current social distancing and work-fromhome orders may well diminish the need to pay our friends and relations in the near term.

eCommerce card not present

In the short-term, eCommerce spend on travel and discretionary items has tanked, however online ordering of grocery goods and fresh foods is up globally. Discretionary spend, such as fashion, will recover once people are again allowed to physically interact. Grocery and fresh food ordering online will be a new habit – whether for home, work or locker delivery, or click and collect. Although it may not maintain at COVID-19 levels, this will likely fuel more rapid long term growth in eCommerce retail spend.

Monthly payments

The economic impact of potential (or actual) unemployment, of recession and of media noise about depression, will all make consumers more wary of both the sustainability of companies that they deal with and their own ability to pay in annual large lump sums. We predict this will lead to a preference for annual payments to be made monthly (already a trend before the crisis), and not necessarily by auto direct debit (as consumers may wish to retain control). In addition, this preference may lead to consumers demanding that they are not penalised with any surcharge for paying monthly.

Noting that, just as the decline in ATM use accelerates the volume of electronic payments, so too does monthly payment . . . 12 transactions rather than one.

New products

Adversity is often the mother of invention, so it is likely that we will see a range of new electronic payment products, use cases and services being created.

Opportunities only for the card rails?

An emphatic “No”. As noted above, online real-time payments over the NPP may be accelerated – whether by Osko, other overlay services or by ‘pay anyone’ (previously via direct entry) payments growing faster. The increased volumes allowing the NPP to become less expensive per transaction.

Perhaps a trend towards mobile phone payments will improve the use case for NPP payments on your phone at POS, enabled by QR codes? Notwithstanding, we do expect that there will be even more new overlay service activity that takes advantage of the NPP.

Conclusion – How might Covid 2020 Pandemic Change the Way We Pay?

The current COVID-19 crisis will see payment volumes drop sharply as economic activity stalls. Within the remaining payment activity, the mix of payments will change:

- The reduction in cash and ATM usage that has been occurring over many years will accelerate into a steep decline

- The cross-border usage of payment cards will drop to low levels

- Use of contactless card and mobile payments will rise

- Use of remote services/ordering, and with them the associated remote payments (eCommerce, in-app, other online), will increase

- A move to monthly payments.

Depending upon the length of the crisis, many of these changes will become habitual and are likely to outlast the short term impact of the virus – such that the retail payments mix in the Australian economy will be altered forevermore.

Disclaimer: The opinions expressed in this article are the author’s own and do not necessarily reflect the view of Indue. The Initiatives Group has advised participants in the payments market since the 1990’s – including issuers, acquirers, third-party processors, technology providers and associations. The Initiatives Group has a strong relationship with Indue, and can help participants in the payments sector generate more value from their markets and customers. To find out how, please get in touch.

Sources:

1 A Oxford University study in 2014 found that the average European banknote contained 26,000 bacteria which could be potentially harmful to a person’s health; and market research has found the majority of European consumers rank physical money as being more unhygienic than the hand rails on public transport

2 https://www.fastcompany.com/90480199/how-companies-can-support-their-employee-caregivers-duringthecovid-19-outbreak

3DSecure 2.0 – eftpos Enters the Fray

3DSecure 2.0: eftpos Enters the Fray

With the introduction of 3DSecure, eftpos has continued its journey to ensure its cardholders have the highest standards in transactional security without adding unnecessary friction to the cardholder experience.

3DSecure – Securing Payments

3DSecure (3Ds) is a security protocol that provides an additional layer of protection for cardholders and merchants alike for card-not-present (CNP) eCommerce transactions. It is used to authenticate the cardholder whilst undertaking a payment, ensuring that the person conducting the transaction is indeed the cardholder.

The purpose of the 3DS protocol is to facilitate the exchange of data between stakeholders – the merchant, cardholder and card issuer. The objective is to benefit each of these parties by providing the ability to authenticate cardholders during a CNP eCommerce purchase, reducing the likelihood of fraudulent usage of payment cards.

Issuers of Visa and MasterCard card products have already been exposed to 3DSecure 1.0 and its recent version 2.0 successor in the form of ‘Visa Secure’ and ‘MasterCard SecureCode’, respectively.

Indue is finaliaing a program of work with all of its Visa card issuing clients to upgrade Visa Secure version 1.0 to version 2.0. Version 2.0 introduces the requirement to have dynamic cardholder verification (i.e. one-time password via SMS) instead of static cardholder verification (i.e. cardholder identity questions).

eftpos enabling 3DSecure 2.0

Based on industry feedback and continual working groups, eftpos has undertaken the same initiative as the other card schemes and has commenced the process of establishing its own 3DSecure requirement. The scheme is currently working on finalising its solution design and technical specifications.

Indue has advocated to eftpos that its 3DSecure solution be compatible with the other card schemes’ solutions – namely Indue wants to ensure that eftpos’ final solution design allows the reuse of what its card issuing clients have already built to support the other schemes’ solutions. This would ensure that eftpos cardholders benefit from the same security protections as other scheme cardholders whilst leveraging the effort already expended to build a 3DSecure solution.

Implementation Timeline

The eftpos 3DSecure 2.0 solution is currently in planning phase. eftpos is presently working with existing Access Control Servers (ACS), who provide the authentication solution software for issuers and merchants for 3DSecure, to finalise their own set of requirements.

eftpos have yet to confirm a set date for their finalised 3D Secure solution, but have advised that by October 2020, there will be a liability shift favouring those parties who have opted to enroll and implement the new security solution. The same strategy was previously employed by other card schemes in order to promote adoption and ensure that both parties within a transaction (merchant and card issuer) are protected against card fraud.

Once Indue has received eftpos’ detailed requirements for 3DSecure functionality, we will undertake further analysis to understand the changes and engage all of our affected eftpos Card Issuers to initiate a project for implementing the solution.

Tokenisation – What is it and can it beat payment fraud?

Tokenisation – What is it and can it beat payment fraud?

Tokenisation seems to be one of the key buzzwords in the payment industry at the moment. However, what does this concept really mean and how does it benefit payments made today?

What is Tokenisation?

Tokenisation is a method of protecting sensitive data by replacing it with an algorithmically-generated number referred to as a ‘token’. In the payments world, tokenisation is commonly used to replace debit and credit card numbers in an attempt to prevent card fraud.

Under this form of tokenisation, a cardholder’s Primary Account Number (PAN) is replaced by a random number that is not linked to the card number prior to processing a transaction through the payments network. This process assists in mitigating the risk of exposing sensitive card data to unauthorised individuals or software that could potentially exploit the data by fraudulently duplicating the card details. It also prevents merchants from storing the PAN in databases, which are targets for hackers. Tokens cannot be decrypted or reverse-engineered. The only relationship between the original card number and its associated token number resides within the Token Service Provider.

What is a Token Service Provider?

A Token Service Provider (TSP) is a service provider that issues tokens, manages the lifecycle of tokens and stores the payment credentials associated with the tokens. TSPs can be an independent third party from the payment network or can be the actual card scheme (i.e. Visa, MasterCard, eftpos). TSPs must conform to strict security and privacy specifications defined by the global payment schemes and fall within the PCI-DSS compliance requirements.

Tokenisation in the Industry

Tokenisation takes many forms within the payments industry. One of the most prevalent uses of tokenisation is within the Mobile Payments space. When a cardholder provisions their payment card within an Apple or Google mobile wallet, the request is sent to the appropriate TSP to tokenise the card number. The token is then sent back to the mobile wallet for activation. The cardholder’s actual card number is never stored on the mobile device and as such cannot be extracted for misuse. All subsequent mobile transactions will use the token number as the payment credentials.

Tokenisation for in-app purchases is also on the rise due to its convenience. Some in-app purchases leverage the mobile payment functionality whereby the token stored on the mobile wallet is used to make a purchase within the phone application. An example of this would include purchasing tickets on the Ticketek app and instead of inputting credit card details, the user is able to select the Apple Pay option, which references the credentials stored within the mobile wallet. Not only does this option provide an easy streamlined purchase journey, it also removes any sensitive data from the transaction.

Tokenisation for in-app purchases is also on the rise due to its convenience. Some in-app purchases leverage the mobile payment functionality whereby the token stored on the mobile wallet is used to make a purchase within the phone application. An example of this would include purchasing tickets on the Ticketek app and instead of inputting credit card details, the user is able to select the Apple Pay option, which references the credentials stored within the mobile wallet. Not only does this option provide an easy streamlined purchase journey, it also removes any sensitive data from the transaction.

Tokenisation for card-on-file online purchases is also becoming more common given the recent occurrences of global data breaches. Wawa, a popular convenience store chain in the United States, confirmed in late 2019 the discovery of malware on their payment processing servers. The malware captured credit and debit card numbers, cardholder names and expiration dates. Card-on-file tokenisation protects a cardholder’s card credentials stored at online merchants with whom the cardholder frequently make purchases. Netflix holds the card credentials of all its customers for the purpose of charging the monthly subscription fees. The streaming service provider has recently undertaken a significant exercise of tokenising as much of its database as possible as a means to mitigate the risk of data breaches. As more online merchants migrate to tokenisation, the prevalence of card data breaches will hopefully decrease as well. Given that a new unique token is generated for each retailer, a security breach at one retailer will not compromise the security of the token data at another retailer.

Payment Account Reference – Providing a holistic view

Although the use of tokenisation enhances the security of digital payments, it also presents a challenge. If a cardholder’s card credentials are tokenised for use within Google Pay on an android phone, Apple Pay for an iPad and Netflix for monthly subscription payments, it becomes a one to many relationship. One single PAN is now linked to several tokens across different systems and platforms.

As only the TSP has the original data linking the PAN to the multiple tokens, the lack of visibility makes it difficult for other parties such as merchants to have a consolidated view of all transactions performed by the cardholder and subsequently provide value-add and compliance services. An example of this is the provision of fraud and anti-money laundering monitoring services. To provide the most effective service, there is a need to identify transactions on an aggregate card level to better assess customer behaviour and payment trends.

As a means to provide a consolidated view, some card schemes have introduced the use of a Payment Account Reference (PAR). According to a recent white paper published by EMVCo, a global entity facilitating worldwide interoperability of secure payment transactions, a PAR is a ‘non-financial reference assigned to each unique PAN and used to link a Payment Account represented by that PAN to affiliated Payment Tokens’. PAR is passed in the transaction message to the merchant so that they can reference this field when performing customer level analysis.

EMVCo affirms that this is a long term solution that will solve the issue by linking together disparate card-based and token-based transactions without compromising on security. Although this is the recommendation of EMVCo, it is the responsibility of the card payment schemes to adopt this concept and implement it into their respective payment ecosystems. eftpos is introducing support for PAR in the near future.

Resources:

Insight: The changing face of consumer payments in Australia

Insight: The changing face of consumer payments in Australia

Our guest writer, David Oierholm, Director of The Initiatives Group, sheds light on the changes and trends of consumer payments in Australia.

The ways in which consumer payments in Australia are made is often likened to a train system comprised of the “rails” that carry the carriages (the payment systems), and the “carriages” that carry the passengers (the individual payments).

The media will have us believe that the payments landscape in Australia is constantly and rapidly changing. To an extent this is correct – but this is all about new “carriages” rather than “rails”.

Furthermore, simply because there are new ways to pay on offer, it does not mean that we all immediately change the way we pay. For example, it took well over 5 years for both BPAY and (much later) contactless card payments to become mainstream.

In Australia, there has only been one new set of rails introduced in the past 25 years (The New Payments Platform (NPP), 2018)

The Way We Pay

It is about trends, and long-term ones at that. The following graph shows how the ways we pay (our use of the rails) have changed over the past 16 years, exhibiting slow movements and not, as many media commentators would suggest, overnight leaps.

The trends are clear – cash (as proxied by ATM withdrawals) and cheque usage are on the decline, and fast becoming the minority of transactions. Electronic payments continue to increase. Cards now account for more than 50% of all payment transactions, with the growth in debit card activity far outstripping credit card since 2007. It is now quite normal to pay for a morning coffee using a card – not so long ago a $3.50 purchase would have been made with cash.

Will cash and cheques ever completely disappear? It is more likely that cheques will disappear, but only when the industry and/or regulator set a termination date – otherwise someone, somewhere will keep using them. However, the ability to access and use cash is considered critical for members of society who may be unbanked, and for remote residents where electronic payments may either be unavailable or inconsistent. Even in those economies closest to being cashless, such as Sweden, there are government requirements for the economy not to become cashless – at least not until no one is left behind or disenfranchised.

In 2019, the San Francisco Board of Supervisors passed a law requiring that all bricks and mortar retail businesses must accept cash – this even includes the Amazon Go stores (more about them later). This move is to make sure that the city’s poorest residents are not shut out of access to basic goods and services. Whereas “cash not accepted” signs are common in shops in Sweden.

The Rails

The rails for electronic payments in Australia include the card rails (Visa, Mastercard, Amex, eftpos), the rails for direct entry and direct debit payments known as BECS (Bulk Electronic Payment System), the real-time payments rails operated by New Payment Platform Australia (NPP) and the international bank to bank transfer rails (SWIFT). The only one of these sets of rails that has been introduced within the last 25 years is the NPP, launched last year.

(Source: The Initiatives Group)

The Carriages

What runs on the rails is where the new action has been, as a plethora of “veneers” have been placed on top of the payment rails, giving the perception that the movement of money has changed. What has changed, and greatly, is the consumer interface, which has become more convenient, simple to use, frictionless and seamless. But, as noted earlier, just because a new way to pay is being offered there is no guarantee that it will be used.

Mobile Wallets (Mobile Payments)

Mobile wallets such as Apple Pay, Google Pay and Samsung Pay, otherwise known as “The Pays”, have arguably received more media headlines than any other payments related topic over the past few years. Despite this, it is estimated that they represent fewer than 5% of card present transactions, albeit that there now seems to be some acceleration in the adoption rate.

Requiring a credit or debit card to fund a transaction, The Pays operate on the Visa, Mastercard, American Express and, to a lesser extent, the eftpos rails. They have been offered in Australia since 2015 when Apple Pay was launched with Amex.

Even though some would describe it as simply a new “form factor” – a contactless payment (now over 90% of card present transactions) using a phone rather than a plastic card – the rollout through the payments industry has been slow. A popular hypothesis is that using your phone currently offers little benefit over using a plastic card – that is, there is no value added.

In addition, there has been significant reticence amongst the major banks to fund the fees payable to Apple Pay, which also comes with the limitation of no other application being able to access the NFC interface on the iPhone. However, as of today the only major Australian bank that does not offer Apple Pay (considered the vanguard of The Pays) is Westpac, so it is felt that the current low usage rates will increase to more significant levels over the next few years, assisted by use on mass transit.

A different type of mobile wallet where you can “pre-fund” your account prior to purchase (or link to a “top up” source of funds) is particularly popular in China, and increasingly so throughout Asia. AliPay and WeChat Pay both from China are prime examples.

When making purchases, these systems run on their own sets of rails with the transaction driven by a QR code interface (overcoming Apple’s NFC quarantine). This has permitted significant growth in electronic payment acceptance due to the simple and low cost set up for the payee. However, to fund the account, money is transferred from the user’s card or bank account.

This means the funding uses existing payment rails. To date the use of QR codes in payments in Australia has primarily been limited to visiting Chinese tourists. Australians are already well served by NFC contactless payments, so, whilst there may be more value-adding capability within a QR code, there is little incentive for consumers to change.

Another popular wallet, although not so much in mobile format (at least not in Australia), is PayPal. Created as a payment wallet to make secure online transactions, the PayPal wallet can be instantly funded by a credit or debit account, or pre-funded. An interesting contrast is that in the US keeping funds in a PayPal wallet is popular, whereas in Australia it is not.

In-app Payments or “payments in the background”

Popularised by the success of the Uber rideshare app and the “just get out of the car at your destination and walk away” payment experience, in-app payments are the topic of a separate whitepaper published by The Initiatives Group.

Sometimes criticised for making it too easy for consumers to overspend as they do not have a “transaction moment” to reconsider their purchase, in-app payments are growing even faster than e-commerce. Prime examples include Uber – familiar to most of us; Grab, which dominates carshare in South East Asia, and which is now promoting its payment service in its own right as “GrabPay”; and the Hey You (Beat the Q) café pre-order and payment aggregator app.

In the USA, Starbucks is prolific enough to have its own pre-order and payment app, which accounts for a significant proportion of their sales and is integrated with the Starbucks Loyalty program. Further loyalty integrations are underway. For example, in the USA you can use American Express Membership Rewards points to pay for your Uber ride. Amazon is taking the in-app, seamless shopping and payment experience to the nth degree, (possibly out of the budgetary capabilities of most retailers) with its Amazon Go “no lines, no checkout” concept stores, it is extreme but an insight into what is already possible!

In Australia, Woolworths is currently trialling “Scan & Go” with selected Woolworths Rewards loyalty members in Sydney – it is a variation on Amazon Go, where shoppers scan items when they take them from the shelf and then just tap off when leaving the store. This is important, as Woolworths and Coles are able to move the market: it was really not until they adopted the NFC technology that contactless payments became commonplace in Australia.

The Form Factor

Many innovations on the existing payment rails are actually changes in the form factor. As noted earlier, mobile payments are, for the most part today, simply the ability to use your phone to make a contactless card payment, rather than use the physical card itself.

Other new form factors include smart watches, including the Apple watch, Samsung Gear watches, as well as Garmin and Fitbit with Garmin Pay and Fitbit Pay respectively. Similarly, there are wrist bands and tabs attached to watch bands, even sunglasses and jewellery, such as the Bankwest Halo Payment rings. Current opinion is that these “wearables” will become popular, but amongst niche groups rather than the general population – for example waterproof bands and rings for swimmers, surfers, runners and cyclists.

BPAY and Pay Anyone

BPAY and Pay Anyone (Direct Credit on internet banking or a banking app) are payment methods that use the BECS Direct Entry system. Both allow for bank account to bank account transfers five days a week (excluding Public Holidays), with banks transferring funds 5 times per day (but not necessarily posting them to accounts that frequently).

Reliable, secure and low cost, however it is possible that a transfer can take some time to occur or appear in the receiving account – if the transfer is made late on Friday afternoon and is to a bank that is not posting intra-day settlements it may not be until the following Tuesday that the funds appear in the recipient’s account.

Whilst BPAY volume continues to grow, BPAY now somewhat competes with itself as the provider of the first “overlay” service “Osko” for the NPP, which allows real time payments between consumers and businesses via BSB and account number or with a registered PayID (mobile number, email address or ABN) linked to their bank account. Further, a number of Financial Institutions have and are moving their Pay Anyone / Direct Credit transactions onto the NPP rails, instead of using BECS.

P2P (peer-to peer) Payments

Particularly popular in geographies as diverse as the USA and China (perhaps due to the antiquated and previously limited payment systems available), P2P payments allow instant payments between consumers – splitting the bar tab, paying your share of the rent, getting money to the kids quickly, etc.

Venmo (now owned by PayPal) in the USA and WeChat Pay in China are prime examples. Both allow instant payments between other Venmo or WeChat Pay users from a pre-funded wallet. Perhaps they could be considered alternative rails, however, funding still comes from the existing rails transfer methods as these are linked to accounts.

In Australia, BeemIt allows P2P payments between BeemIt users, requiring only a Visa or Mastercard debit card for registration. Interestingly, BeemIt accesses bank accounts by using Visa and Mastercard for the authorisation messaging, then uses the eftpos rails to achieve the instant funds transfer.

As with many new ways to pay, BeemIt has not (yet) become popular in Australia as it has yet to gain sufficient penetration or ubiquity, and perhaps does not solve a significant problem that Australian consumers have (given the various other ways that they have to pay).

Real-time Payments

The establishment of real time payments platforms, moving and posting money between accounts 24×7, such as Australia’s NPP, is a major global trend. The UK has had “Faster Payments” and Singapore “FAST” for some time. More recently, Malaysia “DuitNow” and TCH (“The Clearing House”) in the USA have introduced real time payment platforms.

The NPP was launched in February 2018, the first new payment rails in Australia for 25 years (the prior launch was BECS in 1993). The NPP is an initiative that was primarily driven by the Reserve Bank of Australia, following its review of innovation in payments, and is co-owned by 13 banking organisations. It allows for real time payments between bank accounts.

To date, it has been held back by a somewhat uncoordinated introduction through the banking system. Whilst over 2 million PayID’s have been registered, use of the Osko payment “overlay service” has been relatively limited. This is likely to change once all banks deliver the range of features available, more entities register PayID, and business applications such as “Request to Pay” and a central consent management platform are delivered (effectively allowing Direct Debit transactions to be introduced by the NPP).

To date, it has been held back by a somewhat uncoordinated introduction through the banking system. Whilst over 2 million PayID’s have been registered, use of the Osko payment “overlay service” has been relatively limited. This is likely to change once all banks deliver the range of features available, more entities register PayID, and business applications such as “Request to Pay” and a central consent management platform are delivered (effectively allowing Direct Debit transactions to be introduced by the NPP).

Even Sweden’s “Swish” success story has taken almost 7 years since its establishment in 2012 to reach a total of 1 billion transactions through the system.

Use cases range from instant P2P payments, to real time payment of employee wages, superannuation, even to the ability to safely buy/sell a used car privately on the weekend without the need for cash transfers or bank cheques.

(Image Source: Osko.com.au)

Real-time / Faster Cross Border Payments

Cross border account to account payments have primarily been the domain of Swift and its 165 member banks. Even if the origin or destination banks are not members, the 165 banks can act as “correspondent” banks to route funds into the recipient country and currency, then onto the recipient bank. It is reliable, but can be slow, opaque and relatively expensive. The Swift rails also enable currency transfer services such as Western Union.

Faced with the emerging faster cross border payment challengers, such as crypto currencies, Ripple, Visa B2B Connect, and Visa and Mastercard acquiring FX transfer platforms, Swift has been developing faster, lower cost transfer products to enhance its existing rails. Swift GPI (Global Payment Innovation) is now conducting faster cross border payment trials, and is poised for rollout network wide.

Swift, which also provides the distributed switching platform for Australia’s NPP, is also testing its involvement in integrating the different real-time payments platforms between countries.

Thought too slow and expensive (today) for domestic payments, cryptocurrencies and distributed ledger technology is of interest for the future of cross border payments, although there is a long way to go. For example, Bitcoin transactions can occur at between 10-20 transactions a second (versus Visa at up to 56,000 per second), and crypto currencies are infamous for the volatility of their value in fiat.

However, the announcement in June 2019 of the Libra Foundation, with its bundled currency backed blockchain based “stablecoin”, and the Facebook developed Calibra payment wallet (planned to be the first wallet for Libra transactions) has generated significant excitement and debate. Whether or not is succeeds (or even permitted to launch by regulators), it raises the possibilities of western “bigtech” finally entering the payments (and broader financial services) category, and the possibility of a truly global currency that transcends fiat currencies and national borders – at the same time, reaching one of the world’s broadest social network audiences.

Will Libra run on new rails? Within the Calibra wallet this is likely, but Libra ultimately still needs to be funded from some other electronic source such as a bank account or card (even if unbanked users pass cash across the counter at “agent” locations). Indeed, it has been suggested that, to reach merchants for POS transactions, it may use the Visa and Mastercard rails.

There will be many legislative hurdles to overcome, and, in developed countries such as Australia with highly developed payments systems, there remains the question of what real problems are Libra and Calibra really trying to solve (maybe remittances?).

Use cases range from instant P2P payments, to real time payment of employee wages, superannuation, even to the ability to safely buy/sell a used car privately on the weekend without the need for cash transfers or bank cheques.

Buy Now, Pay Later (BNPL)

With millions of customers in Australia, the USA and soon in the UK, “I’ll AfterPay it” is becoming a familiar expression. AfterPay, Zip Money, Humm and SplitIt have become particularly popular amongst millennials – Afterpay claims 69% of its users are 18-35 years old.

New way to pay, on new rails? No. Latitude and Flexigroup have been offering interest free payment plans for decades, and products such as Afterpay rely on debit and credit cards to make initial payments and subsequent repayments.

However, Afterpay and its cohort have tapped a rich vein of new business – millennials who are not migrating to credit cards, with a short-term low value instalment payment product, tuned initially for online purchases and delivered digitally. Merchants with a sufficient margin structure to absorb the 4-6% fee, see the additional sales as a boon in what is currently a tough retail environment. Add to this a group of BNPL businesses, those delivering similar products to small businesses, such as ProspaPay.

Conclusion – Consumer Payments in Australia

The adoption of electronic payments by consumers and businesses in Australia continues apace, pushing cheque and cash transactions (although not the amount of cash on issue) into a relatively steep decline. Consumer payments are dominated in volume by card-based transactions, but the format of these is starting to become “buried” under layers of “veneer” interfaces, many of which rely on card-on-file for their funding source.

To the consumer, these veneers look like “new ways to pay” and certainly deliver the more convenient and seamless experience that people seem to be seeking. But underneath, the funds are moving between the payer and payee accounts as they have always done.

The new rails provided by the NPP will not generate any new transactions in the market, but will take volume from existing systems. For the sake of efficiency and the economy, one hopes that the NPP will accelerate the decline in cash usage and lead to the termination of cheques. But it will also take volume from Direct Entry and card payments. Just as Swish has entered ecommerce and the point of sale market in Sweden, once the cost of NPP transactions reduces (as it should with volume growth) then one would expect it will also appear in the online and POS environments.

The increasing use of electronic payments in Australia should see the overall cost of payments as a percentage of GDP decline and the tax take through GST and income tax rise – both of which are beneficial for the country.

Disclaimer: The opinions expressed in this article are the author’s own and do not necessarily reflect the view of Indue. The Initiatives Group has advised participants in the payments market since the 1990’s – including issuers, acquirers, third-party processors, technology providers and associations. The Initiatives Group has a strong relationship with Indue, and can help participants in the payments sector generate more value from their markets and customers. To find out how, please get in touch.

eftpos: Making Digital In-roads (Digital Acceptance Pilot)

eftpos: Making Digital Inroads (Digital Acceptance Pilot)

eftpos, in conjunction with Indue clients, has successfully conducted a digital transaction in the Digital Acceptance Pilot program.

It has been quite a busy year for eftpos. With the increase in the number of banks offering merchant choice routing, (which enables merchants to choose to route transactions via their preferred network) and enabling mobile payments via the eftpos network, eftpos has definitely advanced its value proposition for its customers. One key initiative that is critical to the eftpos network ecosystem is its Digital Acceptance Pilot program.

This aligns with eftpos’ commitment to updating its product suite to continually meet changing merchant and consumer needs.

Digital Acceptance Pilot Program

Digital development will continue to be a key focus for eftpos over the coming year as Australians change the way they pay for goods and services.

This functionality enables eftpos cardholders to make online purchases at participating merchants using their eftpos card,. This is an unprecedented capability for the scheme.

eftpos collaborated with all parties within the transaction journey (Issuers, Acquirers, Switch Processers, Merchants and other service providers, including Indue) to develop and implement this new capability. Indue undertook a program of work with its eftpos clients, which commenced in 2018, to assist with the implementation of the required system changes to support online eftpos transactions.

First-Ever Online eftpos Transaction

In July 2019, eftpos coordinated a production validation program between card Issuers and participating Merchants to validate the new digital functionality changes. Three of Indue’s clients participated in testing and successfully made online transactions with selected merchants. The hard work undertaken by multiple stakeholders, including Indue and Indue’s clients, in the Digital Acceptance program was finally realised when the first-ever online eftpos transaction occurred during this validation. Previously, eftpos cardholders were unable to conduct online transactions using their eftpos cards.

This one transaction has fundamentally changed the payment landscape. Now eftpos joins the other card schemes in the digital arena.

eftpos Enters the Digital Arena

In September 2019, eftpos began a Digital Acceptance Pilot Test program which has since seen more successful transactions made between several Merchants and Issuers. With the new functionality now validated in the live payments environment, this will have significant implications on the balance of power between the major card schemes due to the fostering of healthy competition.

As more merchants become enabled to accept online eftpos transactions, the industry will no doubt see some movement of transactional volume from other card schemes to the eftpos network.

Indue is extremely excited about the implications of this new capability for its clients – a richer cardholder experience through the expansion of their product’s reach.

API Economy

With around 50 million eftpos-enabled cards in market, eftpos aims to help card Issuers create innovative, bespoke and secure payment experiences for their customers. The company is building an API gateway, with the first APIs expected to be in production early in the new year, potentially bringing new opportunities for innovation across the eftpos network.

Insight: The Disruptive Threat

Insight: The Disruptive Threat

By now, everyone in Financial Services has seen a headline with dire warnings of “disruption” – by one of the Internet Giants like Amazon or Facebook, or by a regional FinTech startup in Australia. Industrie&Co’s Lukas Bower explains how financial services providers can respond to the disruptive threat.

How can you Respond?

The disruptive threat is indeed real, but how does a mid-tier financial services provider respond?

Many mid-tier providers in Australia focus on a specific region, industry, or some other slice of the broader market. To combat disruption, your solution lies in uncovering and addressing a need that is uniquely important to your specific community of customers.

The “Design Sprint” Approach

If you read the trades, you’ll be aware that customer-centricity is the norm in today’s digital business.

Early customer-centric methodologies focused on the desirability of an idea – exploring whether a customer wants a new feature, by testing an idea with real customers.

As customer-centric approaches have matured, they have expanded to look at technical feasibility and commercial viability as well. This end-to-end exercise is called a Design Sprint – which can be completed in a matter of weeks.

Feasibility & Viability

Feasibility explores your existing technology landscape (CMS, CRM, and any other customer-facing systems), and determines if an idea customers love is technically feasible to implement. Feasibility considers your existing environment – and calls out any technical gaps that need to be addressed. If gaps exist, the feasibility phase tests whether they can be addressed through short Tech Spikes – simple technology tests that prove or disprove whether a technical solution will work.

Viability looks at the idea from a business lens. Will it save more money than it costs to implement? Will it retain more customers? Will it help acquire new customers? How long will it take to implement? What training will your team need, if any, to put the new idea in the market?

Building the Right Thing

At the end of the Design Sprint, your business will have enough information regarding Desirability, Feasibility and Viability to decide whether or not you should invest in an idea – and enough customer feedback to understand how strongly they feel about your proposal.

This ensures your business will invest in building the right thing – and avoid spending time and resources on ideas that don’t deliver customer and business value.

Why This Matters

Your competitors do not have the same direct and unfettered access to your customers that you have. Your access enables you to find out your customers’ unique needs and pains, and tailor your solution to fit – using a Design Sprint.

Building the right thing for your customers is key. Building the right thing makes your business “sticky” by giving your customer base more reasons to remain with you – even with new alternatives emerging in your market.

This article was written by Lukas Bower (@lukasbower) Managing Director at Industrie&Co Australia. As the payment landscape continues to evolve with new technologies, new payment providers and new customer requirements, it has become increasingly evident that financial institutions must ensure they continually assess whether their products and services are meeting the needs of their market.

The implications of ignoring these ‘disruptions’ is the risk of falling behind the masses and losing out to adaptive competitors.

Responding to the Threat

Indue has partnered with Industrie&Co to enable a major Australian retailer to bring an unprecedented product into the Australian market, which is a great example of responding to the ever-advancing demands of the industry.

Interested to learn about how you can compete with industry disruptors? Join Indue’s Chief Commercial Officer, Dave Hemingway as he hosts an audience with Industrie&Co to dive deeper into the practical applications of design sprint methodology.

When

Thursday, November 14th, 11.00am AEDT

Industrie&Co is an Innovation and Technology Consultancy. With offices in Sydney, Melbourne, Hong Kong and Singapore, Industrie&Co helps Financial Services companies identify and build winning product ideas – from Design Sprint through to launch. Industrie&Co has a strong relationship with Indue, and can help implement next-generation payment solutions. To find out how, please get in touch and share your vision with us.

Industrie&Co is an Innovation and Technology Consultancy. With offices in Sydney, Melbourne, Hong Kong and Singapore, Industrie&Co helps Financial Services companies identify and build winning product ideas – from Design Sprint through to launch. Industrie&Co has a strong relationship with Indue, and can help implement next-generation payment solutions. To find out how, please get in touch and share your vision with us.

How consumers are redefining customer experience

How consumers are redefining CX

In their 2019 Global Consumer Insights Survey, PwC introduces the concept of “ROX” as a way for companies to measure their success on the metric of customer experience.

The following article on customer experience first appeared on www.pwc.com.au on 26 Mar 2019. Author Chris Paxton

Customer Experience (CX) Key takeaways

- Customers are embracing technology in their pursuit of online goods and services.

- Brands wanting to increase spend and frequency should focus on the changing nature of customer experience.

- Friction-less interactions that integrate with a customer’s daily life and technology are key.

Is experience really everything? Yes, according to respondents of PwC’s 10th annual Global Consumer Insights Survey (GCIS).

Canvassing more than 21,000 consumers from 27 territories, the survey found consumers the world over want good customer experience when they shop. And what’s more, with the technology they have access to, they can now demand it.

On their wish list is an experience that is curated, channel-agnostic, socially conscious and social-media-powered. For some businesses, this is a tall order, and not one that has gotten enough attention in the past. Gone are the days when a pleasant smile is enough to gain customer favour.

Consumers, with technology at their fingertips, are redefining what good customer experience means.

Living digital

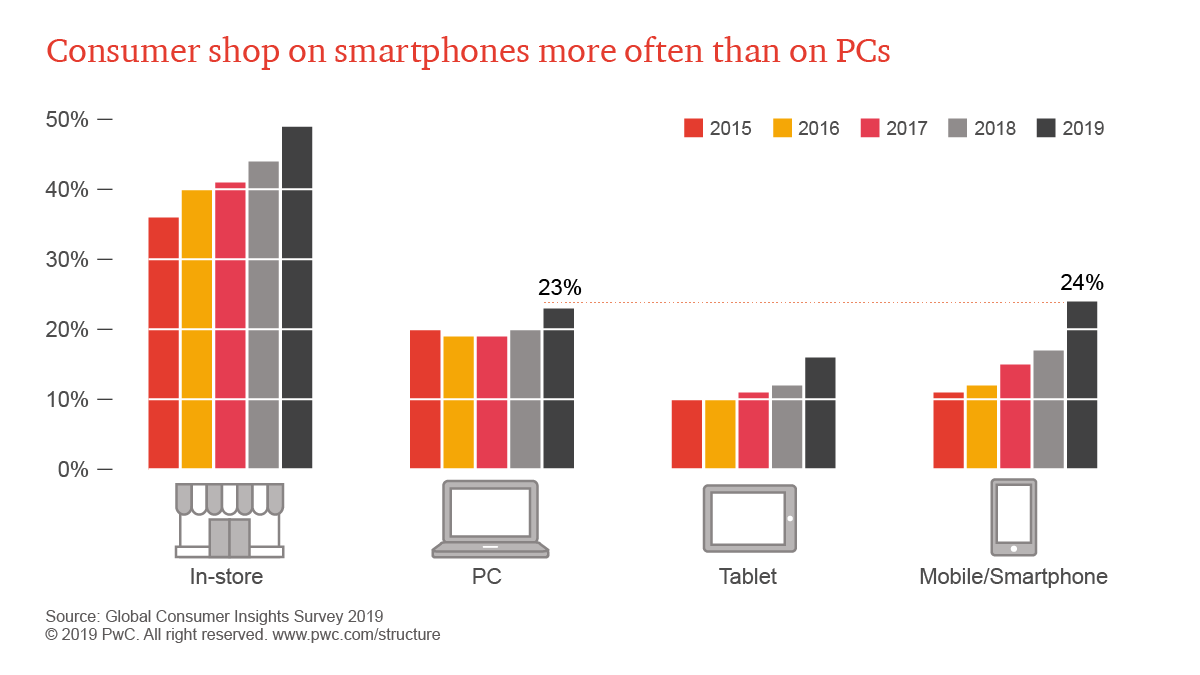

Technology is infiltrating daily life at breakneck speed. Mobiles, tablets and PCs are all being used for online shopping. This year, for the first time since the study has been run, mobiles overtook all other digital devices as the preferred shopping tool. Smartphones were reported as the go-to tech for purchasing, with 24% of respondents using a phone to shop at least weekly. The trusty PC is still close, though falling in favour, at 23% of consumers, while tablets bring up the rear at 16%

Online shopping is now the norm, with only 7% of people saying they never purchase products online.

As anyone who has coached a tech-wary relative on the ease of online banking can attest, people eventually become comfortable with the online experience. Over half of those surveyed paid bills or invoices online in the last year, with similar numbers transferring money. Entertainment, such as streaming movies and TV, is also booming, with 54% watching two to three times a week or more (over half of Gen Z streams daily).

Smartphones are also increasingly being used for payment, particularly in emerging regions where mobile phone use has leapfrogged traditional landline systems. While the technology’s prevalence is different depending on the country, globally, 34% of consumers have paid for a purchase via their mobile in 2018, up 10% on the previous year.

Frictionless shopping

Newton’s first law of motion states that a body in motion will continue to remain in motion until it is acted upon by an external force, that is, until it encounters friction. Customers, it turns out, are much the same. The less friction in their purchase journey, the more they’ll shop, and the more they’ll spend. Thirty-four percent of those surveyed said they shop more frequently due to having used Amazon, suggesting the experience – and likely its ease – encourages online shopping.

Voice assistants, such as Google Home or Amazon’s Alexa, are increasingly relevant to online shoppers with their AI hearts built around predictive, frictionless interaction (even if reality is still catching up with the promise). Nine percent of the global sample said they use the technology weekly or more. As the report notes, however, “as shopping by voice continues to catch on, companies should be thinking beyond mobile to consider how voice technology in homes, cars, and elsewhere will affect customer experience”.

Anything that adds friction will not be looked upon kindly. Click-and-collect functions, already adopted by 42% of Australian retailers, are gaining favour in the US (under the acronym BOPUS, or ‘Buy Online and Pick Up in Store’), but customers need to be helped through the experience before they will trust it – and that’s where employees come in.^

The human-digital touch

While customers want to interact with brands via digital means, this doesn’t mean they want humans out of the picture entirely.

This year, smartphones have proven more popular than PCs when it comes to purchasing online, but in-store shopping is still popular. How can brands manage the mix of in-person and digital experiences?

This year, smartphones have proven more popular than PCs when it comes to purchasing online, but in-store shopping is still popular. How can brands manage the mix of in-person and digital experiences?

In PwC’s Consumer Intelligence Series report on customer experience last year we found that 59% of those surveyed believed that companies had lost touch with the human element by focusing too much on tech. One of the takeaways was that brands needed to have a good mix of technology and staff, and in particular, have tech that empowered employees to provide superior service.This finding is echoed in the current survey, particularly as regards financial services, where only 15% had purchased insurance via a digital channel, only 13% had gotten a loan and only 12% made a financial planning decision. For this industry, and others, more education is required by the customer before they feel comfortable in making a purchase. A blended experience, where in-person interaction is mixed with digital experiences throughout the journey, can prove far more fruitful in these instances.

Dreaming big

When it comes to redefining customer experience, it is also apparent that not only are consumers increasingly more willing to try online purchasing, they’re ready to increase what they do online in other ways. Almost 75% of consumers have installed as many as three health or wellness apps on their phones, and two-thirds of those surveyed are willing to access such services through nontraditional players – such as Facebook, Apple or Amazon.

Health and wellness apps are enjoying wide adoption by consumers – particularly for weight loss and exercise.

Health and wellness apps are enjoying wide adoption by consumers – particularly for weight loss and exercise.

Health is not the only example when it comes to pushing traditional boundaries. Forty-six percent of consumers would like to have, or will consider having, an autonomous vehicle. Fifty-eight percent would consider investing in or using bitcoin or another digital currency.

It’s clear that customers are expanding their digital horizons and, as they explore, their expectations will grow with them. For brands, this means delivering a superior customer experience the entire length of the journey customers take.

Sources

This article was originally published on www.pwc.com.au. For all the insights from the Global Consumer Insights Survey, download the full report here.

^ https://www.abc.net.au/news/2017-08-30/click-and-collect-why-retailers-are-pushing-shoppers/8856504

Trend Report Delves into the Benefits of Mobile Wallet Payments

Trend Report Delves into the Benefits of Mobile Wallet Payments

Speedpay Pulse considers the Impact of the “Mobile Mind Shift”

For many consumers, smartphones are an integral aspect of their lives. According to Pew Research Center, 77 percent of Americans now own smartphones, up from just 35 percent from the organization’s 2011 smartphone ownership survey. As consumers have become more comfortable utilizing their smartphones for everyday tasks, many companies have simultaneously enhanced their pay by mobile wallet capabilities to cater to consumer preference. This offering includes any technology that stores payment card information, whether native to your smartphone, or via downloadable third-party payment methods.

(Source “Speedpay Pulse Trend Reports”)

Transitioning to Digital

According to the Speedpay® Pulse, a consumer billing and payments trend survey of 3,000 U.S. adults responsible for two or more household payments a month, one in four consumers currently use mobile wallet payment methods and nearly half (47.6 percent) of those people use mobile wallet offerings multiple times a week. Due to an increase in mobile wallet usage, retailers have begun offering loyalty rewards and other incentives, and based on their research, these strategies seem to be working. Of those who use mobile payment methods, 82.2 percent report using one to three methods and applications on a regular basis. The numbers were almost the same for non-payment items, as 80 percent of those who use mobile wallets also take advantage of options such as digital tickets and boarding passes.

Due to the ease and convenience of these offerings, mobile wallets are becoming the new normal, which could eventually remove the need for consumers to pack a physical wallet and smartphone each day.

The Impact of the Mobile Mind Shift

The Impact of the Mobile Mind Shift

The growing adoption of smartphones and apps has essentially shifted consumer attitudes. Due to this change, mobile wallet payment options have become a necessity for companies, especially because this particular type of transaction is gaining traction for bill pay. Many consumers find that mobile wallet payments provide a simple, convenient payment option, unlike traditional cash and check payments. According to their most recent report, approximately 33 percent of consumers said they would consider using a mobile wallet to pay bills in the future. The top two reasons reported were speed (55 percent) and convenience (51 percent).

Weighing the Option of Adopting Mobile Wallet Payments

Many companies are still reluctant to adopt mobile wallet payments; however, in order to meet the needs of consumers, they should consider implementing mobile wallet offerings. By catering to consumer preference and interacting with them via their smartphones, companies can help ensure an easier and more seamless payments experience. Additionally, the reminders offered via mobile wallet are very beneficial and provide a convenient way to remind their customers to pay. Many mobile wallets have the capability to send monthly statements and notifications directly to a customer’s smartphone, which offers an additional communications channel. Lastly, if companies consider adopting mobile wallets, they will be able to increase self-service and digital engagement among customers, which can lead to a decrease in paper usage and overall operational costs.

Mobile wallet payments will continue to gain popularity in the foreseeable future. Whether customers are paying their bill with a physical debit/credit card or via mobile wallet, it’s recommended that companies constantly communicate with their customers to provide them with a convenient and seamless payments experience.

Article first published 19 February 2019, www.paymentsjournal.com Author Alexis Blackstead

Source: www.paymentsjournal.com Read full article here. To learn more about consumers’ mobile wallet payment preferences, download the Speedpay Pulse Trend Report here.

The NPP turns 1 this week (New Payments Platform)

New Payment Platform turns 1 this week

This week marks one year from the launch of the New Payments Platform (NPP) in Australia, and its first overlay service, Osko, which delivered the ability for payments to be made in real time.

With 75 banks now offering NPP, more than 2 million PayIDs registered and month-on-month growth around 20%1, it’s clear financial institutions are recognising the benefits this platform offers their customers. This week, the NPP turns 1!

“Indue is one of the 13 founding members of the NPP initiative, and we’re proud to see the NPP adopted among our diverse client base, including a mix of smaller banks supporting retail customers. It’s been an incredible year of innovation in payments and we would like to congratulate all involved in reaching this milestone anniversary.” (Indue CEO Derek Weatherley)

And our customers’ customers are enjoying the benefits. Just like how this Queensland Country Credit Union customer realised his dreams of owning a boat in an (almost) instant thanks to Real-time payments.

How Australians are using real-time payments 2

Osko by BPAY is the NPP’s first overlay service being used by consumers, businesses and fintechs. Since launching, Australians are enjoying the benefits of real-time payments and paying family and friends in under a minute, 24/7, even on weekends and public holidays.

“People transfer money at all times of the day – after dinner, on the weekends, at a footy match or cinema or even when buying something on Gumtree. Increasingly, they are expecting to access their money immediately. Most people will notice they have made an Osko payment when they get their payment receipt in online banking.” (Mark Williams, Chief Strategy Officer of BPAY Group.)

BPAY reports that Osko payments are not just limited to consumer to consumer transactions, with 30% of payments are to, or from, businesses and between businesses.